Most fintech growth teams think about push notifications as a channel. “What should we send this week?” “How do we increase open rates?”

Wrong framing.

The best fintech push strategies don’t start with the notification. They start with the user. Where is this person in their journey? What do they need right now? What’s the one thing we could tell them that would make their financial life better in this moment?

Push notifications in fintech aren’t a broadcast channel. They’re a relationship progression.

This guide walks through every stage of the user lifecycle — from the first app open to win-back — and shows exactly what to send, when to send it, and why it works. No generic advice. No real app names. Just the strategy.

TL;DR

- 76% of new users convert within 7 days when engaged via push in their first week

- 9.35% CTR with narrow behavioral segmentation — 14x better than broad blasts

- 56% engagement uplift with rich push formats — yet only 8% of marketers use them

- 31% conversion lift when push + email + in-app are orchestrated in a single journey

- 5 notifications/week is the cliff — beyond this, uninstalls spike

- The highest-performing fintech apps match notification type to lifecycle stage, not just audience segments

Stage 1: Permission & Onboarding — Earning the Right to Notify

The journey starts before you send a single notification. It starts with the opt-in.

The Permission Prompt Problem

Triggering the system permission prompt on first app open — before the user has experienced any value — costs you up to 50% of your potential opt-in base. Finance apps already lead all industries in push opt-in rates (96% on Android), but iOS is a different story. And even on Android, a premature prompt trains users to ignore you from day one.

The rule: earn the right to notify before you ask for the right to notify.

What the Best Fintech Apps Do

They delay the prompt until after a meaningful action:

- After the first deposit or transaction

- After completing KYC verification

- After the first portfolio view or savings goal setup

And they contextualize the ask:

“Turn on notifications to get real-time alerts when your investments move”

is a fundamentally different ask than a generic system prompt before the home screen loads.

Onboarding Notifications That Work

Once permission is granted, the first 7 days are critical. Users who receive timely push notifications in their first week are 76% more likely to convert than those who don’t.

Here’s what to send in the onboarding window:

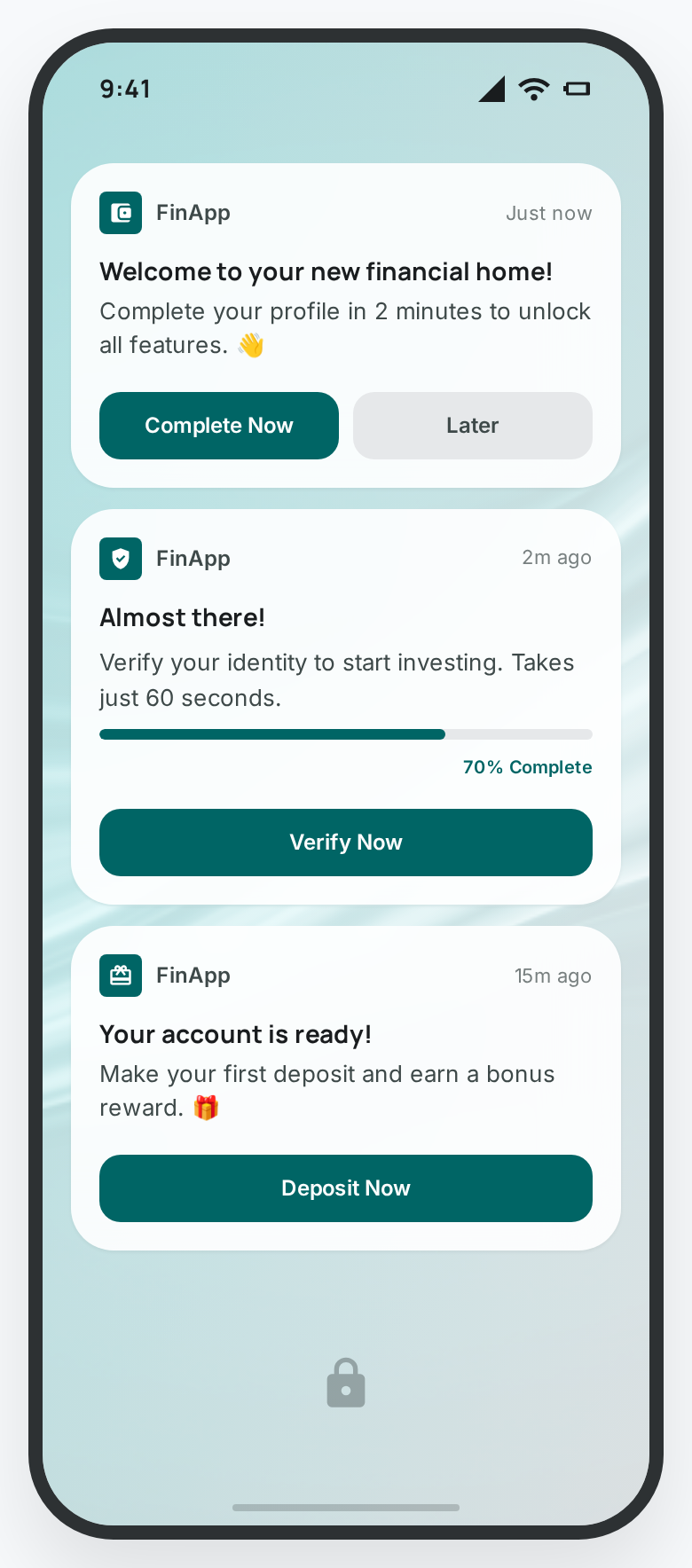

Day 0 — Welcome + next step:

“Welcome to your new financial home! Complete your profile in 2 minutes to unlock all features.”

Keep it warm, specific, and action-oriented. Tell them exactly what to do next and how long it takes.

Day 1-2 — KYC/verification nudge:

“Almost there! Verify your identity to start investing. Takes just 60 seconds.”

Include a progress indicator when possible (“You’re 70% done”). People are far more likely to complete a process they’ve already started.

Day 3-5 — First action prompt:

“Your account is ready! Make your first deposit and earn a bonus reward.”

Tie the first action to a reward or benefit. The goal isn’t just activation — it’s creating the first habit loop.

Best Practices for This Stage

- Time-bound the onboarding sequence. If KYC isn’t completed within 48 hours, shift the messaging from “complete your setup” to “here’s what you’re missing.”

- Use progress indicators. Incomplete progress is psychologically harder to abandon than a fresh start.

- Limit to 1 notification per day. Onboarding users are forming their first impression of your communication style.

Stage 2: Activation & First Value — Making the App Indispensable

The user is set up. Now the job is to demonstrate value so clearly that they can’t imagine going back.

The Activation Window

The first 30 days determine whether a user becomes a retained customer or joins the silent majority who install and forget. Apps that send event-triggered notifications in the first week see 15% more users making repeat transactions.

What to Send

Personalized transaction confirmations:

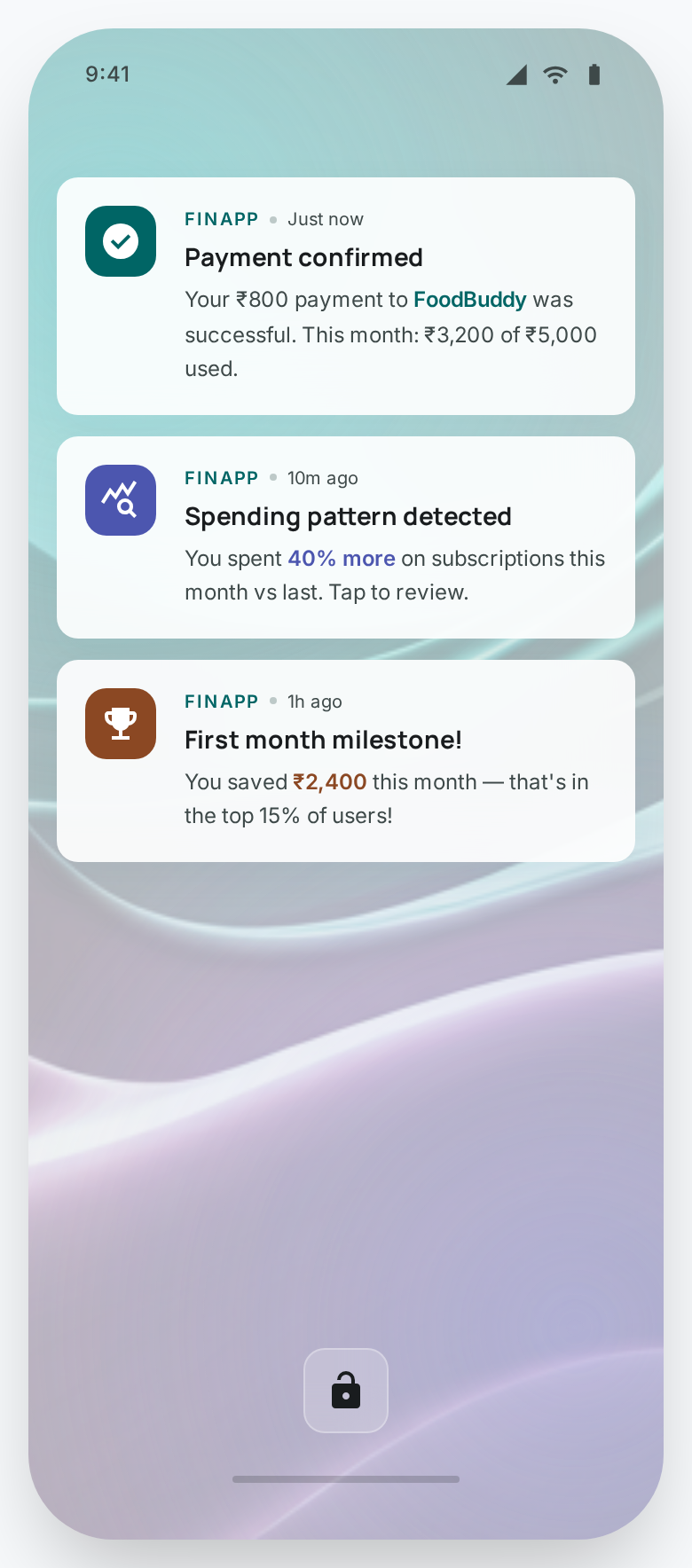

“Your ₹800 payment to FoodBuddy was successful. This month: ₹3,200 of ₹5,000 food budget used.”

Don’t just confirm — contextualize. Every transaction notification is a chance to reinforce the app’s value as a financial awareness layer, not just a payment pipe.

Smart financial insights:

“You spent 40% more on subscriptions this month vs last. Tap to review.”

This is the notification no traditional bank would send. It requires pattern detection and the courage to surface unsolicited but genuinely useful information. It’s also what turns a fintech app from “another payment tool” into “my financial advisor.”

Milestone celebrations:

“You saved ₹2,400 this month — that’s in the top 15% of users like you!”

Social proof + achievement + personalization. This is the notification that gets screenshotted and shared — turning push into earned media.

Deep Personalization Beyond First Name

Name-insertion is table stakes. The winners use behavioral personalization:

- Merchant-specific transaction summaries

- Salary pattern detection (“Your salary is 2 days late compared to last month”)

- Percentile rankings against similar users

- Budget tracking tied to spending categories

The gap between “Hi {first_name}” and this level of contextual intelligence is where real engagement lives. Dynamic personalization — pulling specific loan limits, offer amounts, or spending summaries into each notification — is what separates a 2% CTR from a 9% CTR.

Timing Matters as Much as Content

Match notification type to time of day:

- 9-10 AM — Financial check-in (market open, balance check, portfolio updates)

- 1-2 PM — Post-lunch browse (payment reminders, bill due dates)

- 7-9 PM — Evening wind-down (spending summaries, investment reviews, rewards)

Send informational notifications in the morning, transactional in the afternoon, engagement in the evening.

Stage 3: Retention & Engagement — Building the Habit Loop

The user has activated. They’ve experienced value. Now the challenge shifts: how do you keep them coming back without becoming noise?

The Frequency Cliff

5 notifications per week is the danger zone. Beyond this, uninstall rates spike. But the real trap is counting frequency by channel in isolation.

A user receiving 4 pushes + 3 emails + 2 SMS = 9 touches per week, even if each channel looks fine by itself. Global frequency capping across all channels is non-negotiable.

Gamification: Open Loops, Not Closed Messages

The most engaging fintech notifications don’t just inform — they create open loops that pull users back into the app.

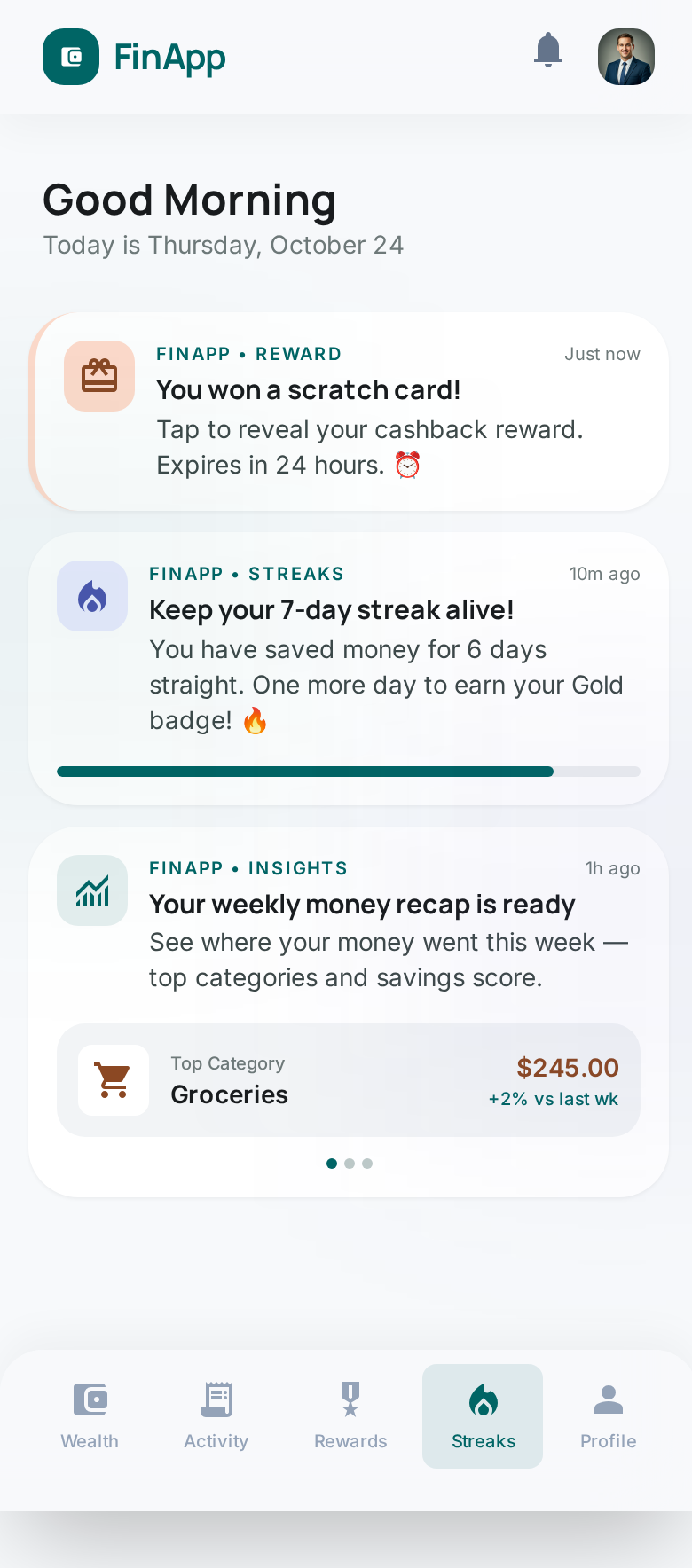

Scratch cards with expiry timers:

“You won a scratch card! Tap to reveal your cashback reward. Expires in 24 hours.”

The timer creates urgency without feeling spammy because the user earned the scratch card through an action. FOMO-driven, but earned — not manufactured.

Streak mechanics:

“You’ve saved money for 6 days straight. One more day to earn your Gold badge!”

An incomplete streak is psychologically harder to abandon than a fresh start. Streaks convert habitual actions into identity-level behavior (“I’m the kind of person who saves every day”).

Variable rewards (the slot machine effect):

The most sophisticated behavioral hooks in fintech use variable-reward patterns. Stamp collections, randomized cashback amounts, and mystery rewards all trigger the same dopamine loops that make slot machines compelling — but tied to financially healthy actions.

The genius is the open loop. An incomplete stamp collection or unrevealed scratch card is harder to ignore than a discount code. Don’t close the loop in the notification — create an itch that only opening the app can scratch.

Rich Push Formats: The 56% Uplift Most Teams Ignore

Rich push notifications — carousels, countdown timers, images, progress bars — deliver a 56% engagement uplift. Yet only 8% of marketers use them.

The low-hanging wins for fintech:

- Carousels showing top spending categories of the week

- Countdown timers on cashback offers or scratch card expiry

- Progress bars for streak milestones or savings goals

- Live tracking notifications (credit card delivery, loan disbursement progress)

- Multi-product carousels for cross-sell (insurance, loans, credit cards)

Rich push is the biggest single-lever improvement most fintech growth teams haven’t pulled yet.

Give Users Control

The apps with the lowest churn rates are the ones that let users define the relationship:

- Per-category notification toggles (transactions, promotions, insights)

- Quiet hours and DND mode

- Frequency preferences (daily digest vs real-time)

Users who customize their notification preferences almost never turn notifications off entirely. A dimmer switch beats a light switch.

Stage 4: Monetization & Cross-Sell — Push as Revenue Driver

Once a user is retained, push becomes a direct revenue tool — but only if you’ve earned the right through the previous stages.

Contextual Cross-Sell

The best cross-sell notifications feel like helpful suggestions, not ads:

“You’ve saved ₹50,000 this quarter. Ready to put that money to work? Explore mutual fund SIPs starting at ₹500/month.”

This works because it’s:

- Triggered by a real milestone (savings threshold)

- Personalized to their actual balance

- Specific about the next step (SIP at ₹500/month)

- Not a generic “check out our new feature” blast

Push-to-In-App Continuity

The highest-converting strategies treat push as the first frame of an in-app experience, not a standalone message:

- Zero gap between tap and destination

- No splash screens or home page redirects

- Deep link directly to the relevant screen

- The notification taps straight into a pre-filled flow

Push-to-checkout integration — a notification with a pre-filled payment amount that takes the user directly to the confirmation screen — delivers the highest push-to-action completion rates in fintech.

The metric that matters: Not push open rate, but push-to-action completion rate. If 40% open but only 5% complete the intended action, the push-to-in-app handoff is broken.

Journey orchestration that stitches push to in-app experiences (a push tap triggers an in-app modal, bottom sheet, or gamification experience) can dramatically reduce the drop-off between tap and action. Tools like Plotline make this push-to-in-app stitching possible without engineering effort for each campaign.

Priority Routing for Critical Notifications

Not all notifications are created equal. A payment failure alert is existentially different from a promotional cashback offer.

The best fintech infrastructure teams implement priority queuing:

- P0 (Critical): Payment failures, security alerts, fraud warnings → always delivered, multi-channel fanout

- P1 (Important): Transaction confirmations, bill due dates → real-time, single channel

- P2 (Engagement): Promotions, insights, rewards → batched, frequency-capped

Missing a P0 notification costs real money. Burying it under P2 promotional noise is a failure of infrastructure.

Stage 5: Reactivation & Win-Back — The Second Chance

Users go dormant. It happens. The question is whether your win-back strategy makes them feel valued or pestered.

The Dormancy Signal

Start the win-back sequence when behavioral signals indicate disengagement:

- No app opens in 7-14 days

- Declined from daily active to weekly to inactive

- Stopped mid-funnel (started KYC but didn’t complete)

What to Send

Win-back with tangible value:

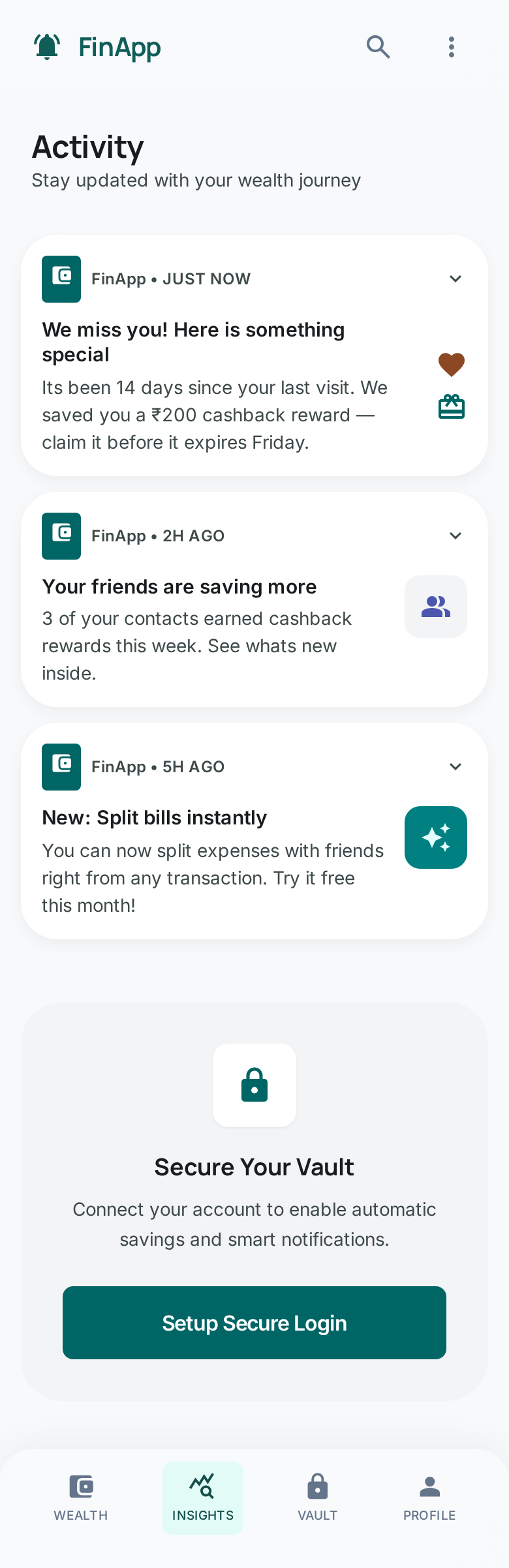

“It’s been 14 days since your last visit. We saved you a ₹200 cashback reward — claim it before it expires Friday.”

The expiry creates urgency. The specific reward amount (not “a special offer”) creates clarity. And “we saved it for you” creates a sense of loss aversion.

Social proof nudge:

“3 of your contacts earned cashback rewards this week. See what’s new inside.”

Peer activity is one of the strongest reactivation triggers. “Your friends are doing something you’re not” cuts through notification fatigue.

Feature announcement:

“New: Split bills instantly. You can now split expenses with friends right from any transaction.”

Dormant users often leave because they hit a friction point. New features that remove that friction are a genuine reason to come back — but only if the notification is specific about what changed and why it matters to them.

The Win-Back Sequence

A single notification rarely reactivates a dormant user. Structure a 3-touch sequence:

- Day 7 of dormancy: Soft re-engagement (what’s new, what they’re missing)

- Day 14: Incentive-based (specific reward with expiry)

- Day 21: Social proof or FOMO (peer activity, limited-time feature)

After the third touch with no response, reduce frequency to monthly. Respect the silence.

The Measurement Framework: Beyond Open Rates

Most teams stop at delivery rate and open rate. The full funnel has 5 stages, and each has distinct failure modes:

Sent → Audience targeting, segment misconfiguration

Delivered to device → FCM/APNs token issues, uninstalled apps, device restrictions

Displayed → OS-level suppression, notification grouping, DND mode

Tapped → Weak copy, wrong timing, notification fatigue

Action completed → Broken deep links, slow load times, friction in the destination flow

The metric hierarchy:

- Push-to-action completion rate — the single most important metric

- Revenue per push sent — ties notification strategy directly to business outcomes

- Unsubscribe/uninstall rate per notification — measures whether you’re creating value or destroying it

- Time-to-action — how quickly users act after receiving the notification

The DPDP Act: Preparing for India’s Consent Deadline

India’s Digital Personal Data Protection Act sets a consent deadline of May 2027. For push, this means explicit, purpose-specific consent for personalization-driving data.

What this means for growth teams:

- Audit your data pipeline now. What user data powers your personalization? Map every attribute to its consent basis.

- Build granular consent flows. “Notifications about your spending” vs “promotional offers” need separate opt-ins.

- Document your consent chain. Can you prove when and how a user opted in?

Apps already practicing consent-first design — clear opt-in flows, granular preference centers, contextual permission prompts — will be least disrupted. Apps relying on blanket permissions will face significant re-architecture.

Putting It All Together: The Push Notification Lifecycle Map

Here’s a summary of what to send at each stage:

Onboarding (Day 0-7): Welcome → KYC nudge → First action prompt. 1/day max. Focus on completion, not promotion.

Activation (Day 7-30): Transaction confirmations → Financial insights → Milestone celebrations. Event-triggered, deeply personalized. This is where you prove the app’s value.

Retention (Day 30+): Gamification rewards → Streak mechanics → Rich weekly recaps. 2-5/week with global frequency capping. Give users control over preferences.

Monetization (Ongoing): Contextual cross-sell → Push-to-in-app journeys → Priority-routed alerts. Only after trust is established. Push as the first frame of an in-app experience.

Reactivation (Dormancy signals): Win-back rewards → Social proof → Feature announcements. 3-touch sequence over 21 days. Respect silence after that.

The Bottom Line

The single biggest mistake is treating push as a broadcast channel. Push interrupts whatever the user is doing — reading, watching, sleeping. That interruption had better be worth it.

The second biggest mistake is treating all lifecycle stages the same. An onboarding notification and a win-back notification serve fundamentally different purposes and should be crafted accordingly.

Segment ruthlessly. Personalize deeply. Time precisely. Use rich formats. Cap frequency at both channel and global levels. And always make the notification the beginning of a valuable experience, not a dead-end message.

In fintech, where the product is someone’s money, trust is the whole game. Every notification either builds that trust or erodes it. There is no neutral.

FAQs

What is the ideal push notification frequency for fintech apps?

Research shows 2-5 push notifications per week is the sweet spot. Beyond 5 per week, uninstall rates spike significantly. But this must be measured across all channels — a user receiving 4 pushes + 3 emails + 2 SMS = 9 touches, even if each channel is under its individual cap. Implement global frequency capping across all channels.

How do I improve push notification opt-in rates for a fintech app?

Delay the permission prompt until after a meaningful user action (first transaction, portfolio view, savings deposit). Contextualize the ask — explain exactly what notifications the user will receive. Apps that follow this approach see up to 50% higher opt-in rates compared to prompting on first app open.

What are rich push notifications and why should fintech apps use them?

Rich push notifications include media elements like images, carousels, countdown timers, and progress bars. They deliver a 56% engagement uplift compared to plain text, yet only 8% of marketers use them. For fintech, the highest-impact formats include spending category carousels, cashback timer countdowns, savings goal progress bars, and credit card delivery tracking.

How should push notification strategy differ by user lifecycle stage?

Onboarding notifications should focus on completing setup (KYC, first deposit) with 1/day max frequency. Activation notifications should prove value through personalized insights and milestones. Retention notifications should create habit loops through gamification and streaks. Win-back notifications should offer tangible rewards with expiry dates and social proof. Each stage has different goals, copy styles, and frequency norms.

How do I measure push notification success beyond open rates?

Track the full funnel: Sent → Delivered → Displayed → Tapped → Action completed. The most important metric is push-to-action completion rate — it measures whether the entire push-to-in-app journey works, not just whether the notification was opened. Also track revenue per push sent and unsubscribe rate per notification type.

Can push notifications be personalized with financial data?

Yes. Leading fintech apps use behavioral personalization — merchant-specific transaction summaries, salary pattern detection, budget tracking, and percentile rankings. Dynamic personalization tools like Plotline’s Liquid Tags pull user attributes directly into notification content at scale — displaying specific loan limits, spending summaries, or offer amounts in each notification.

Ready to build push notification experiences that drive real engagement at every lifecycle stage? Book a demo with Plotline to see how fintech apps orchestrate push-to-in-app journeys across the full user lifecycle.